Trésor-Eco

Review of Public Finance Forecasts for 2023 and 2024

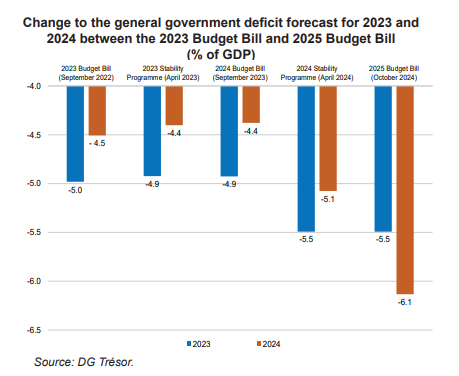

The 2023 general government deficit stood at −5.5% of GDP compared to a forecast of −4.9% in the 2023-2027 Public Finance Planning Act. This difference essentially concerns aggregate taxes and social security contributions, for which the elasticity in relation to economic growth was at a record low. This decline has also significantly affected the projection for 2024 which was revised to −6.1% in the 2025 Budget Bill, versus −4.4% in the Initial Budget Act.

The economic and public finance forecasts for 2023 and 2024 were drawn up amid much uncertainty with highly volatile energy prices, a very high inflation rate and unprecedented monetary policy tightening.

For 2023, while real growth was closely aligned with the forecast (0.9% vs 1.0%), high levels of inflation provoked more substantial revisions of nominal growth, that was initially projected at 4.6% in autumn 2022 then at 6.8% a year later, and which ultimately stood at 6.3%. For 2024, real growth, that was first forecast at 1.4%, was revised downwards to 1.1%, and the nominal growth forecast was reduced from 4.0% in autumn 2023 to 3.5% a year later as it was affected by the faster-than-expected fall in inflation.

The 2023 general government deficit was –5.5% of GDP (–5.3% excluding the change of base year for the national accounts by Insee, the National Institute of Statistics and Economic Studies), compared to the projection of –4.9% in autumn 2023. The 2024 deficit figure has not yet been finalised: the most recent official forecasts were for –6.1 % of GDP, following a projection of –4.4% in autumn 2023, that was revised to –5.1% in April 2024. These revisions are significant but not unheard of from a historical standpoint.

In 2023, the spontaneous growth in aggregate taxes and social security contributions, i.e. without factoring in discretionary measures, was much lower than that of nominal growth (2.6% vs 6.3% for nominal GDP), in contrast to 2022 which was an exceptional year. Such a contrast was anticipated as early as July 2022 but its scale was much larger than projected. Central government expenditure was lower than forecast unlike local authority expenditure.

In 2024, revenue from aggregate taxes and social security contributions was subject to major reassessments due to unexpected events in 2023 that were heightened by the delayed functioning of corporation tax and income tax. It was also slowed by lower nominal growth in GDP that was less driven by private domestic demand, and which had an impact on VAT revenue. In addition, there was a surprisingly high level of local authority expenditure whilst central government expenditure is expected to be lower than provided for in the 2024 Initial Budget Act due to management measures introduced during 2024.

Update

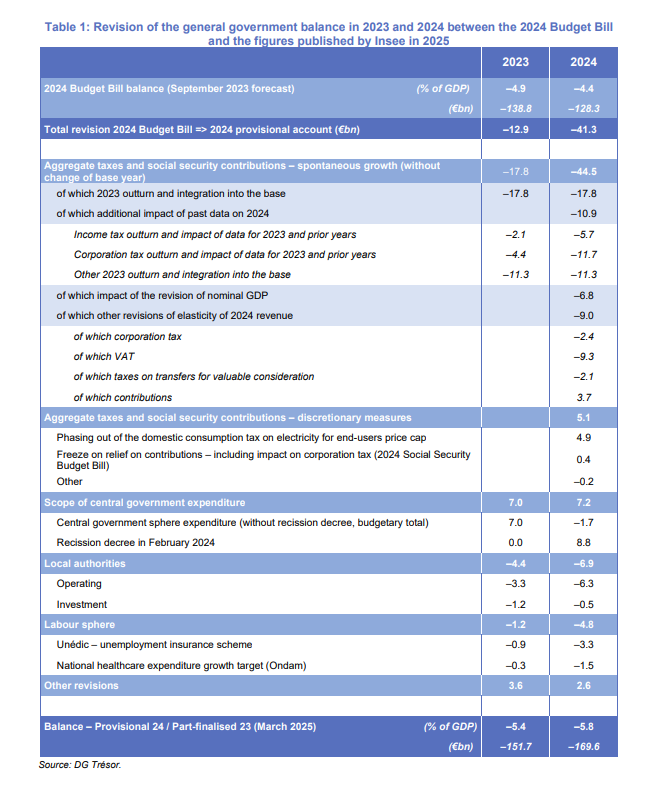

Following the publication by Insee, the National Institute of Statistics and Economic Studies, of the general government accounts, the 2024 general government deficit was ultimately −5.8%, that is to say 0.3 points of GDP more than the projection used in the 2025 Budget Bill and on the basis of which this edition of TrésorEconomics was produced in January 2025.

Revisions constitute an overall improvement of roughly €9.5bn and essentially concern:

• local authority expenditure (+€6.5bn), which turned out to be lower than expected when the 2025 Budget Bill was being prepared, due to a slowdown in this local expenditure starting in autumn 2024. For instance, local authorities’ investment expenditure rose 7.6% in 2024 compared to the 13.2% increase forecast in the 2025 Budget Bill, which was based on the latest accounting data from summer 2024. Operating expenses rose by 3.5% but this was still significantly less than the 4.6% projected in October 2024.

• central government expenditure (up €3.4bn), was less than forecast in autumn 2024 owing to a budget outturn that was even lower than estimated in the Initial Budget Act.

• the 2023 deficit was also revised to −5.4% of GDP, i.e. up 0.1 points compared to the provisional account published by Insee in May 2024.

Table 1 relating to the revision of the general government balance in 2023 and 2024 between the budget bills for 2024 and 2025 has been updated as follows :