Trésor-Eco

What Do the Financial Savings of French Households Finance?

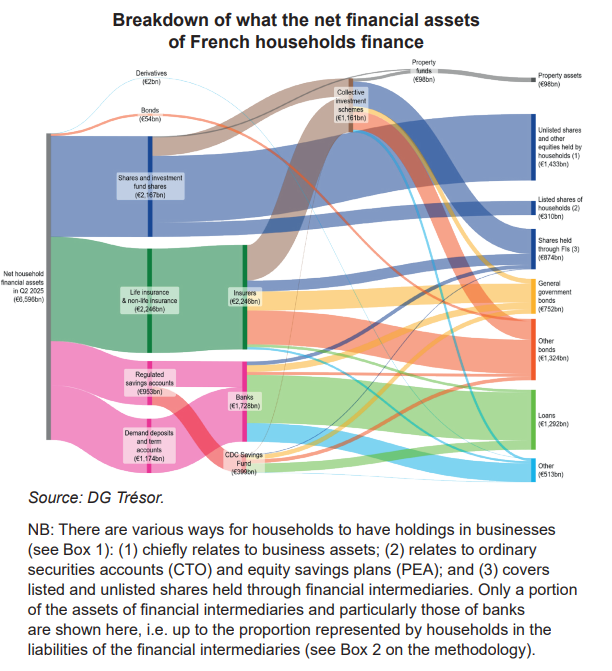

This paper gives a breakdown of the financial assets of French households based on their end use in the economy. Some of these financial assets directly finances businesses, whilst others are invested through financial intermediaries to be used to finance the economy (loans, shares, bonds). For each €10 in financial assets, €4 is allocated to equities in businesses, €3 to bonds and €2 to loans granted to households and businesses.

Net assets of French households primarily comprise property but also include a diverse range of financial assets which are a reflection of households’ longstanding appetite for liquid, secure assets. Financial assets include low-risk investments (deposits, savings accounts, euro-denominated life insurance products) and higher-risk assets such as financial securities (shares and bonds) that are held either directly by households or indirectly through financial intermediaries (FIs), as well as equity interests in their businesses.

Investments made by households through intermediaries help fund the economy as banks, insurance companies and investment funds use these investments to issue loans and purchase shares and bonds. 60% of these products come from France and 80% from the euro area.

A look-through approach was applied to financial intermediaries to examine what is ultimately financed by household savings. For every €10 of household financial assets, €4 is used for equities in businesses – half of which for business assets – €3 to invest in bonds, of which €1 relating to general government bonds (mostly in France), and €2 to issue loans.

Other stakeholders (particularly businesses and non-residents) also make investments through financial intermediaries that help fund the economy and are not covered in this paper. This paper only covers the financial assets of households, which only represent a portion of the assets of financial intermediaries.