Trésor-Eco

The Artificial Intelligence Value Chain: What Economic Stakes and Role for France?

The structure of the artificial intelligence value chain is a determinant of the innovation landscape. Tech giants play a major role in this landscape given their presence across the value chain. Although new entrants are challenging this status quo, it raises questions about economic efficiency, fair competition and sovereignty. France has major competitive advantages in this race, including data, a skilled workforce and an innovative research ecosystem.

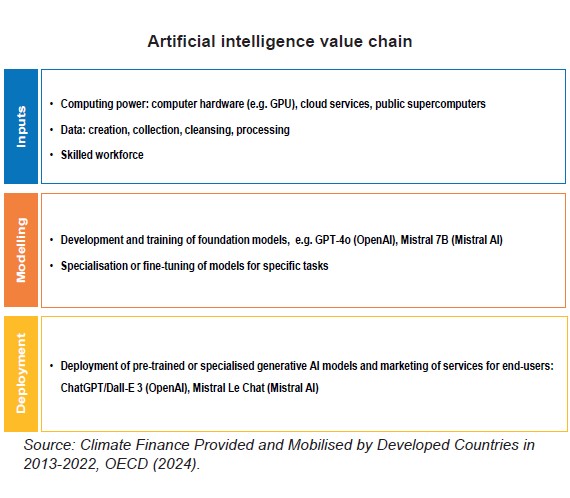

Artificial intelligence (AI) refers to various techniques enabling machines to simulate human intelligence. The AI value chain is divided into three main segments (see Chart below): (i) the inputs required to develop AI systems and services (computing power, data, specialised workforce); (ii) modelling, which includes the development of general-purpose AI models (foundation models) and specialised models; and (iii) the deployment of such models to end-users.

Regarding AI system inputs, France has no major companies on par with the global leaders in the chip manufacturing and computing power rental markets. However, it benefits from a skilled workforce and a thriving innovation ecosystem.

As for AI model development, a few French companies are emerging, but the segment is dominated by the incumbent Big Tech firms established prior to the advent of AI technology. These incumbents enjoy vertical integration thanks to their preferential access to upstream inputs and downstream distribution channels for their AI solutions (e.g. office suite software). They have also partnered with emerging AI firms to integrate AI production processes horizontally.

The dominance of the AI market by a small number of large, already mature firms raises issues of economic efficiency, fair competition, and sovereignty, with the risk of limiting the economy-wide diffusion of AI-related added value and productivity gains.